Our last EVP is now our COO. Since inception in 1993, SEM has had 6 Executives in this group with two retired. Shaun joined SEM on 10/10/2005. After a football career and graduating from the University of South Carolina, Shaun entered the Mortgage Industry as a Loan Officer in our call center and eventually worked his way through the ranks to Office Manager and then Senior Vice President. With a fundamental understanding of our business and the respect from those around him, he took on our newest strategies with passion and commitment. Shaun now works directly with Cal Haupt, Chairman and CEO on SEM’s Social and Media Strategies including various projects with future innovation implications for our industry.

“Shaun is a testament to passion, smart work, and commitment to a common belief. With SEM, Shaun has accomplished more than most in a 30-year career. Instead of moving around like many in our industry, Shaun focused on learning and his skill set. As a result, he made himself invaluable and a trustworthy teammate / large shareholder. I look forward to sharing what I know so he can successfully take on more responsibility in the future. Shaun is not just a smart charismatic guy, he is a good friend and a role model of how to evolve a fantastic career.” Cal Haupt, Chairman and CEO, Southeast Mortgage of Georgia, Inc.

The equivalent of $1 in 1963 is $7.79 in 2018. If you saved your $100 in cash under your mattress in 1963, you would $12.84 of relative cash left.

If you invested $1 a day every day since 1963, you would have $842,416.

Owning a home is an inflation friendly activity. Unlike cash that deteriorates due to inflation, home values rise. With QE1, QE2, QE3 monetary policy since the last financial crisis, inflation should be in the forefront of your personal financial plan.

In today’s economic environment, holding cash is no longer king. A large cushion for the unexpected is always prudent; however, the QE waves heading our way has created an interesting portfolio consideration.

As everyone is starting to realize, the economy is slowing due to the Federal Reserve tightening (raising rates), Tariff battles, and inflation creeping into our daily lives.

What should not be a surprise is we are 10+ years past the last recession. The historical average recovery period is 7 years.

In the mortgage industry we all basically get money from the same place to lend to clients. The competence and service we provide is the differentiator for clients. Unlicensed Bank Originators and Licensed Non-Bank Originators, spend 6-8 hours working with a client. The client spends 15 – 30 years with their advice. Based on the automated underwriting systems (AUS aka LP / DU), the final rate is realized after application. Clients are better served not to worry about an 1/8 or a 1/4 percent up or down. Get the best product for your needs and choose a Loan Originator that is licensed by your state and that focuses on need and not rate. Rate will be what it is based on the verified data in the mortgage application.

Mortgage companies generally compete on the basis of Competence, Service, or Rate. There is a prudent balance for new home buyers. Rates are set by secondary markets and the risk / financial dynamics of the company offering them. Unfortunately many companies are not aware of their risk profile nor the data that impacts their net margins. I call that driving with a blacked out front windshield and no speedometer.

The relationship between the rate a client gets and the rate prior to risk premium and allocation of costs to close generally has a fixed “spread” or margin. There is no special in the mortgage rate market. If you reduce rates past what natural spreads state without cutting costs or lending to higher FICO, LTV, DTI borrowers, there is a consequence down the road. Most Mortgage Originators do not care; however, their consequence is finding a new employer down the road.

In reality, as the economy slows borrowers have higher interest payments on credit cards, their job may fall prey to downsizing, etc. As a result, the risk premium required in pricing mortgage loans should go up not down. Best case, the margin stays the same but the rates will rise proportionately with the market or ignoring sustainable growth will claim its first recessionary mortgage company victim. 366 Mortgage Companies failed https://ml-implode.com/ starting in 2006 (6 years after the recovery) with the capitulation in 2008. Many of you have some of these companies on your resume. Learn from their mistakes.

At the end of every economic cycle I see groups of mortgage companies panic and artificially reduce rates to create a short-term increase in volume. If they did the analysis, they would find this does not change the trajectory of an economic cycle’s impact on mortgage volume. It’s sort of like flapping your arms while falling off a mountain. Flapping may make you feel better but gravity has its own plan that you will not alter the outcome.

My advice based on my learnings from three successful recession crossings, focus on client need and remember origination volume does not pay the bills. Revenue and Competence is the safe bridge to cross uncertain waters.

The product you put your client in is not just another closed loan, it’s the foundation for your client’s family and future.

“Shareholders at Southeast Mortgage are Quantitative Producers in both Sales and Operations, Loyal Teammates, and those who inspire us to be the best. Taking care of our team during their work years and after is our fiduciary responsibility. At the end of the day, I work for 34 of the best bosses a Chairman can have!”

Cal Haupt, Chairman and CEO, Southeast Mortgage of Georgia, Inc.

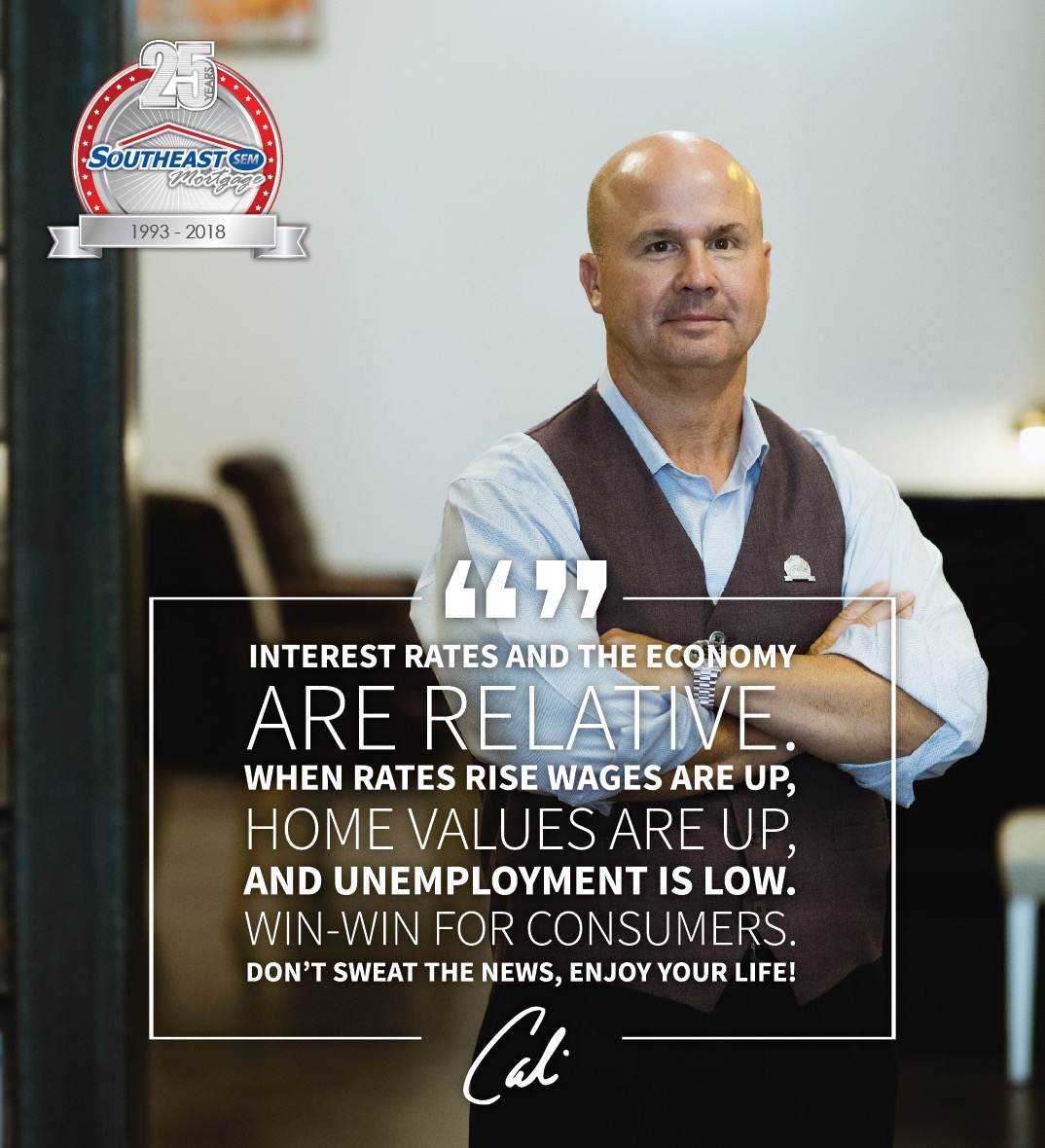

View the Economy this way.

Does a boat run just as fast when its high tide as low tide?

The answer is yes if you pay attention and steer your boat watching your mapping and depth instruments with an experienced eye. Like the tides, the Economy is Relative and steering is required no matter how big you think your boat is or how fast. Without the medium in which a boat operates (water) and the medium a Mortgage Company Operates (Sustained Operating Capital) both can run a ground.

Experience Matters because you do not know you hit ground until its too late.

Cal Haupt, Chairman and CEO, Southeast Mortgage of Georgia, Inc

Technology evolution provides consumers with a choice on how they apply and partners with real & fast 15 minute approvals through innovative systems like GooRu.

Client’s do business with a mortgage company the way they want, not how you want them to apply.

Realtors and Partners need to know their clients are approved prior to showing homes. Southeast Mortgage provides the client and the Real Estate Professional with the technology they need and want. The days of calling an Originator, waiting for a call back, waiting for the client to give the Originator the information, and then getting a pre-approval in day or two is the past.

GooRu approves clients in 15 minutes. Not Pre-qualify, GooRu approves right in the Partners Office or from the Client’s Mobile Device by verifying with the IRS, Banks, and Credit Repositories providing a full AUS decision.

Balancing client need and a Licensed Originator’s career is critical to sustainable success and organic growth.

If you have experienced a decline in volume over the past few months, this video will explain how to grow during a slow down and avoid having to change your employer every few years.

“25 years of success reinforces our philosophy’s TRUTH.”

Cal Haupt, Chairman and CEO, Southeast Mortgage of Georgia, Inc.